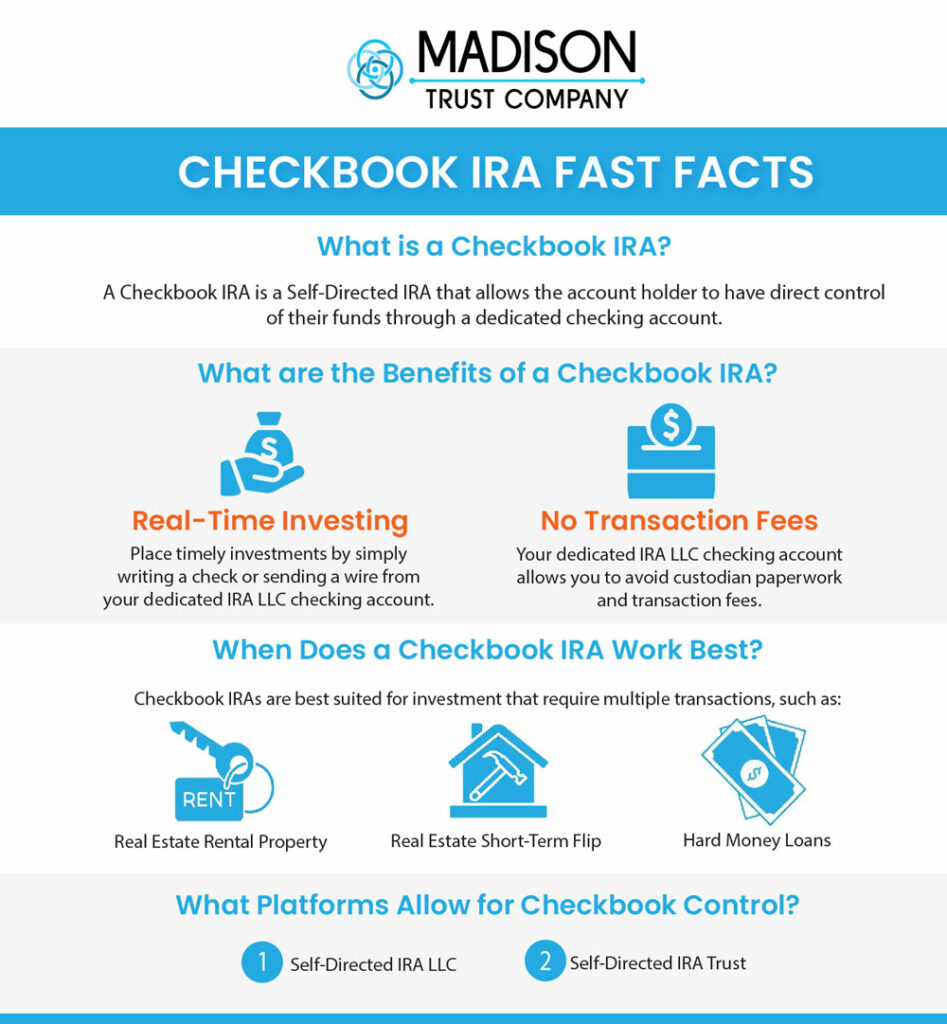

What Is a Checkbook IRA?

Are you considering a Self-Directed IRA for active investments that can help fund your retirement and reduce your reliance on Wall Street? A Checkbook Control IRA, also referred to simply as a Checkbook IRA, might be the best Self-Directed IRA for your interests and goals. Instead of transactions going through a Self-Directed IRA custodian, a Checkbook IRA puts the money in your hands with your bank of choice and a pass-through entity tied to your IRA. You still have a custodian who must manage your initial IRA funding and yearly reporting, but you're in direct control of your funds through your dedicated checking account.

That’s the short answer to the question, “What is a Checkbook IRA?”—but there’s a lot more to learn and know. Here are the basics:

How Does a Checkbook IRA Work?

To set up a Checkbook IRA, you’ll start by opening and funding a Self-Directed IRA with a custodian such as Madison Trust. Then, to gain checkbook control, you’ll need to establish an LLC or trust for your IRA. Typically, an IRA Trust is the faster and more cost-effective option. However, an LLC may be the better choice if you’re planning on purchasing real estate with non-recourse loans, buying property in a state that makes property insurance difficult for a trust to obtain, or considering multi-member investing. An LLC also provides more legal protection than a trust.

Once you have your IRA LLC or IRA Trust set up, the next step is to open and fund a designated checking account for the entity. Having a separate entity and business bank account allows you to write checks and send wire transfers for investments and their ongoing expenses, whereas a Self-Directed IRA on its own requires all transactions to be handled by the designated custodian.

What are the Benefits of a Checkbook IRA?

Between the alternative investments you can make in a Self-Directed IRA and how accessible the funds are when you turn your Self-Directed IRA into a Checkbook IRA, you can gain greater control of your retirement funds and investments. When the money is in your hands, you can move quicker and reduce transaction fees, both when executing on new investments and managing those in your portfolio.

Compared to stressing over the stock market that you can’t control, a Checkbook IRA can be an exciting, empowering, and energizing way to pursue your financial goals. It’s ideal for people who want to be actively involved in specific investments that are best suited for this type of retirement account. With that, we can guess what you’re probably asking next.

When Does a Checkbook IRA Work Best?

The most common use for a Checkbook IRA is to buy and manage rental properties. Paying the bills and contractors to keep tenants happy and the property in top shape is very check-intensive, so you’ll likely want checkbook control instead of having to go through (and pay fees to) a custodian for every transaction. A Checkbook IRA may also be good for fixing and flipping houses.

Even if you’re a passive investor, a Checkbook IRA could be right for you if you’re making multiple investments. When we crunch the numbers, we find that the Checkbook IRA, despite the additional setup costs of an LLC or trust, can save on fees for those Self-Directed IRA holders who make four or more lump sum investments. For this reason, hard money loans are another investment type that’s suitable for a Checkbook IRA.

3 Things to Keep in Mind

Before you open a Checkbook IRA, there are a few important points to be mindful of so you can put yourself in a position to succeed:

1. With Control Comes Responsibility

Less involvement from your Self-Directed IRA custodian means more attention to detail from you. A Checkbook IRA is a relatively advanced investment engine that requires time and willingness to learn the rules and requirements so you manage your investments in accordance with IRS guidelines for Self-Directed IRAs.

2. Absolutely No Commingling Funds

Under no circumstances should you cross personal and Checkbook IRA funds, as doing so would result in a prohibited transaction with tax consequences. Personal funds can’t go into your IRA LLC or trust bank account, and IRA funds can’t be taken as compensation or salary. Read about prohibited transactions.

3. It's More Than an Account

It’s your money, your future, and your retirement. To navigate the ins and outs of a Checkbook IRA, choose a custodian with stability, support, and plenty of positive reviews. When you open a Checkbook IRA with Madison Trust, you also get our sister company, Broad Financial, to get you all set up with your LLC or trust so you don’t have to try and figure it out alone. Learn more about our Checkbook IRA and contact us to get started.

Disclaimer: All of the information contained in our website is a general discussion for informational purposes only. Madison Trust Company does not provide legal, tax or investment advice. Nothing of the foregoing, or of any other written, electronic or oral statement or communication by Madison Trust Company or its representatives, is intended to be, or may be relied as, legal, tax, investment advice, statements, opinions or predictions. Prior to making any investment decisions, please consult with the appropriate legal, tax, and investment professionals for advice.