Where Can I Get a Self-Directed IRA? The One Stop SDIRA Shop

Written By: Daniel Gleich

Key Points

- Self-Directed IRAs (SDIRAs) are individual retirement accounts managed and controlled by you as the investor.

- Your investment options with an SDIRA are nearly limitless. You can access alternative assets ranging from various kinds of real estate, precious metals, and beyond.

- It’s considered best practice to perform your due diligence when choosing the Self-Directed IRA custodian that will facilitate transactions for your Self-Directed IRA.

We all start somewhere. When it comes to planning for your retirement, there’s no better introduction than the innovative Self-Directed IRA. This new age investing tool is a type of individual retirement account, granting investors the chance to curate their retirement savings around an alternative asset aligning with their interest. Self-Directed IRAs place two significant financial ventures (investing and retirement preparation) together to create a forcefield designed to potentially defend your future.

If you’re new to SDIRAs, there may be some questions that need addressing. From what you can invest in, to where you can get a Self-Directed IRA, this is your all-inclusive referential guide for SDIRAs. Let’s peruse through the aisles of the Self-Directed IRA Shop:

A Tisket, A Tascket, What Can I Put in My Self-Directed IRA (SDIRA) Basket?

Diversifying your retirement portfolio is a well-recognized practice in the investment realm. Doing so generally safeguards your retirement savings since alternative assets are typically uncorrelated in performance to Wall Street products. This means you’re avoiding the volatility of the stock market’s unpredictability.

With an SDIRA, you can access tangible assets such as real estate and precious metals, to private placements, promissory notes, startups, and more. What’s additionally wonderful about SDIRAs is that they let you personalize your retirement investing experience. It’s possible for you to invest in something connected to your passions, such as a vineyard, theatrical production, music royalties, copyrights of an artistic work, or a patent to an invention you find miraculous.

Prior to embarking on your self-directing journey, consider speaking with a financial advisor and conducting your own due diligence before making any investment decisions.

Peep the Price Tag – You Won’t Be Returning This Item

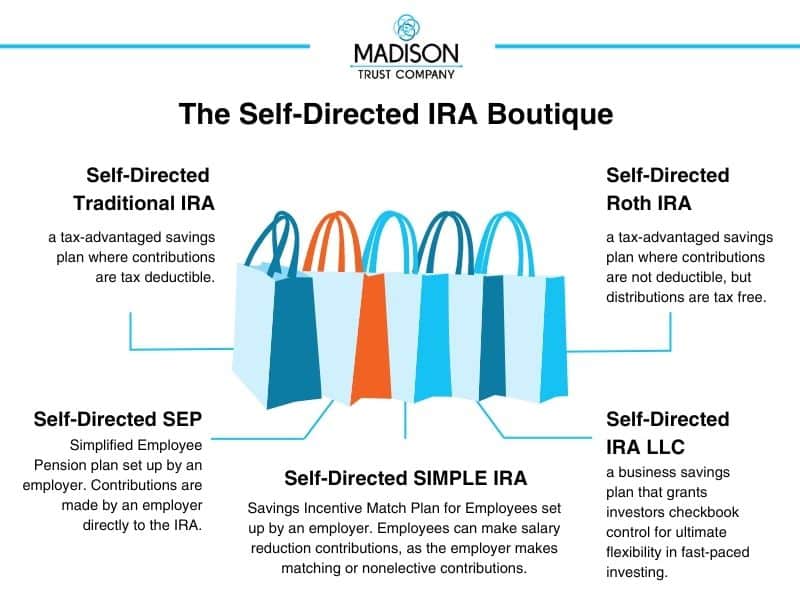

Once you’ve researched and embraced your asset decision, you may want to move to the next step: electing how your self-directed account will develop. By choosing between a Self-Directed Traditional IRA and a Self-Directed Roth IRA, you will assign the funds in your account to grow tax-deferred rate, or tax-free. With a Self-Directed Roth IRA, taking required minimum distributions is not mandated, which can be beneficial depending on your savings goals.

There’s a bundle of varying IRA types to peruse through and consider. By the art of comparison, which one would you throw into your bag?

You Don’t Have to Wait for a Sale to Claim These SDIRA Savings

When it comes to investing with a Self-Directed IRA, you don’t need to wait for a special offer or promotion to pluck the benefits right off the hanger. SDIRAs may offer investors peace of mind as their alternative assets can stand as a hedge against inflation. Whether you substitute your stock and bond investment for an alternative asset, or you invest in an asset alongside a Wall Street product, you can generally reduce your overall investment risk.

Through the power of self-directed investing, almost everything pertaining to your retirement savings is under your control. As the account holder of your Self-Directed IRA, you behave as the manager. Although the IRS requires a SDIRA custodian to facilitate all transactions, these administrative tasks are only performed at your direction.

For those who want the power to invest in real time and are primarily interested in heavy transaction-based investments, you may want to upgrade your IRA to have checkbook control. This gives you the freedom to perform everyday transactions without the need for custodian involvement. An extra incentive is avoiding transaction fees and potentially allocating that money to purchase new investments.

Ready for the Self-Directed IRA Checkout Lane

If self-directing seems alluring and you’re ready to board this investing adventure, you might want to further investigate. The most pertinent decision of them all may arguably be where you can obtain a SDIRA, and who among these options will provide the greatest support. All IRAs must be held by a custodian, such as a bank, authorized trust company, or another entity that’s approved by the IRS to act as an IRA custodian. Your best bet is performing your own due diligence and research to compare the different SDIRA custodians.

Through analyzation of feedback, customer reviews, and word of mouth, we’ve confidently determined the factors most investors are searching for their ideal company to carry. You should ensure your prospective custodians can deliver the following:

- Extensive knowledge of asset classes, IRS codes and proper conduct, prohibited transactions, and the overall workings of a Self-Directed IRA. You will be able to gauge their expertise on these subjects by simply asking them questions.

- Your custodians should continuously display a fast response time. Some investments may be time-sensitive, and it’s imperative that you hear back from your custodian in a timely manner.

- Extraordinary customer service should be prioritized. Self-Directed IRA Specialists should be readily available to take your call and assist you with whatever arises.

Make Madison Trust Your Brand of Choice

Madison Trust’s Specialists undertake precise training so that we can answer any questions you may have about self-directed investing. We strive to provide exceptional service that we are proud to stand behind.

Once you’re committed to self-directing, we are here to walk you through the easy process of opening a Self-Directed IRA. Learn more today by placing a free discovery call.